1. Variation

and how to deal with it

2. The

forces that motivate and demotivate people

The subjects of the first 21

lectures, motivating, staffing and communicating, address the forces that

motivate and demotivate people, i.e. the Theory Z portion of effective

leadership. Forces mean the collection of perceptions, understandings and

misunderstandings that influence the attitude and behavior of people. Lectures

23 – 25 introduced management of processes, part of the control function of

managers, and treated the stand alone topics of managing risk and theory of

constraints. Now we turn to variation and how to deal with it, the central

theme of process improvement and process control. Managing in the presence of

variation is also part of the control function of managers.

W. Edwards Deming claimed that

the inability to interpret and use the information in variation is the main

problem for managers and leaders. (See the book Out of the Crisis by W. Edwards Deming) When there is a problem

with any work process the manager and the employees both must understand when

the manager must act and when employees must act. It is through an

understanding of variation and the measurement of variation that they

understand when and who should take action and, just as importantly, when not

to take action. Thus variation is involved in both improving poor processes and

maintaining good processes.

Variation is just the reality

that actual values of parameters, physical or financial, have some statistical

spread rather than being exactly what we expect, specify or desire. For

example, we may have a budget for supplies of $1000 per month. When we look at

spending for each month it is typically close to but not exactly $1000. Over

time the spending might look like that shown in figure 15.

Figure 15. An example of variation from planned budget by

actual spending.

For our

purposes the definition of variation is deviation from planned, expected or

predicted values of any parameter. The parameter might be financial, as in the

example shown in figure 15, it might be in units of production per day or

minutes per service, or it might be a physical parameter, such as the dimension

of a machined part. Thus variation occurs in all the work processes of any kind

of organization. Therefore, as Deming implied, the effective leader must

understand the information in variation and how to properly manage in the

presence of variation.

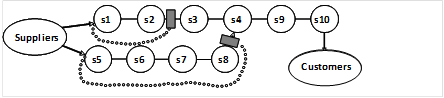

Let’s start by returning to the

work process illustrated in figure 12, the SIPOC diagram. Where might we expect to see variation in a

work process? The answer is everywhere. Deviations from ideal inputs are

variation. Deviations from ideal outputs are variation. Deviations from

expectations in use are variation. Variation in use can be due to either hidden

variation in outputs or unexpected variation in the use environment or the use

process.

Let’s define an effective

process from a customer’s point of view. It is a process that produces outputs

that meet or exceed the customer’s expectations for quality and cost. Customers

can be internal or external to the enterprise or the organization that owns the

process. Customers have stated and unstated expectations. Specifications,

requirements, standards, and contract items are examples of customer’s stated

expectations. Customer’s unstated expectations are typically suitability for

all conditions of use and affordability. Therefore, for the purposes of process

improvement discussions, we can say that an organization’s effectiveness is

determined by the effectiveness of its processes in satisfying its customer’s

expectations. (In general the effective organization must satisfy all its stake

holders’ expectations, including managers, workers, owners and the community as

well as the customers.)

Variation Drives Process

Effectiveness

We can see the effects of

variation by examining an ideal business process (figure 12, an ideal process

is repeated in the top half of figure 16) and a typical process as shown in the

bottom half of figure 16.

Figure 16. Comparison of a

typical process to an ideal business process.

An ideal process converts all

of the supplier’s inputs to outputs that satisfy the customer’s expectations. A

typical process includes inspection steps to ensure that a defective input is

not sent to the process or a defective output is not sent to the customer. The

customer also adds an inspection step because of receiving defective outputs in

the past. If outputs fail any of these inspections the failed item is scrap or

must be reworked. It’s easy to see that the typical process is more expensive,

and therefore less effective, than an ideal process because inspections cost

money and scrap or rework cost money. In a typical chain of processes costs of

failing inspection increases as the work progresses along the chain because

more rework is required if an inspection is failed at processes near the end of

the chain. Thus often the largest cost to the organization is warranty costs

from customer returns. That is the reason for the inspection of the outputs

before they are sent to the customers. The reason these inspection steps are

added is the presence of variation. If there was no variation in the inputs or

the outputs then there would be no need for inspection to find those items

whose variation from ideal is larger than acceptable.

Notice that even the ideal

process has inputs and outputs that exhibit variation but for the ideal process

this variation is within acceptable limits most of the time. We need to define

what we mean by “most of the time”. If there is variation then sooner or later

a product will fail to meet customer expectations if there is no inspection.

(Actually it will happen even with inspection since no inspection is perfect,

i.e. inspection is a process that also has variation.) If the variation is

small enough so that only rarely is there a customer return and the cost of

correcting this return plus the cost of the disgruntled customer is less than

the cost of including inspection then it makes business sense to not have

inspection.

Now I hope the student is

thinking that to make a valid decision to not include inspection takes data to

establish that the variation is sufficiently low. The astute student is also

thinking that collecting such data costs money also, perhaps as much as the

inspection. This is an example of what is meant by a manager needing to know

how to manage in the presence of variation. Next we examine how a manager can

achieve such understanding and make good decisions in the presence of

variation.

Variation is a Statistical

Phenomenon

To understand managing in the

presence of variation we must answer the questions how can the manager decide:

·

when to take action,

·

what action to take and

·

who should take the action?

Managing correctly

in the presence of variation requires the use of methods based on statistics

since variation is a statistical phenomenon. The statistics needed for 85% or

so of a manager’s work is relatively simple and easily learned. The effective

leader and all workers must understand and use these simple methods. However,

there are situations that require more elaborate statistics. Every organization

should have access to at least one person well versed in statistical methods so

that managers and process improvement teams have a resource to check their work

and assist on complex problems. This statistical expert can be a consultant or

a worker that is well trained in statistics.

Here we are

going to briefly look at some of the most important simple methods. As an

example, figure 17 illustrates the daily averages of phone expenses for an

organization plotted for each month of a year.

Figure 17 A graph of an

organization’s daily phone expenses averaged for each month of a year.

Should the manger take action

in response to the March expenses? The June expenses? If action is necessary in

response to the March expenses, whose action is it? The manager’s? The workers?

If the manager is expected to discuss unusual expenses in a weekly or monthly

report what should the manager say about the March and June expenses?

Control charts are a visual

method of answering the questions posed about the phone bills. A control chart

for the phone expenses data from figure 17 is shown in figure 18. You can learn

how to generate control charts later. For now I only partially describe how to

interpret the data in a control chart.

Figure 18 A control chart for

the example phone expense data.

The line with diamond markers

is the same data shown in figure 17. The line with the square markers results

from averaging the data over a whole year. The line with the triangle markers

shows the range of variation of daily expenses for a given month. The two lines

labeled Upper CL and Lower CL are upper and lower control limits, which are

statistically determined from the data set. For the purposes of this

introduction it isn’t necessary to know how to calculate the control limits.

The control chart tells us that, with the exception of the March data point,

the phone expenses are stable, that is they exhibit variation about a stable

sample average, which is not steadily increasing or decreasing. A stable

process is predictable, e.g. frequency of errors, efficiency, process

capability and process cost are predictable. Deliberate changes to a stable process

can be evaluated. Note that some process

improvement literature refers to a stable process as being “in control”.

Variation exhibiting a stable

statistical distribution is due to the summation of many small factors and is

called common cause variation.

Changes to a stable process, i.e. one with common cause variation is typically

the manager’s responsibility but can be the responsibility of trained and

empowered workers. Knowledge workers should be responsible for common cause

variation because they are usually more expert with respect to their processes

than their managers. However, as is described in the next lecture, even

knowledge workers should not be empowered to control their processes before

they have been trained in statistical methods because mistakes can make

processes worse.

Only the data point for one

month, March, falls above or below the two control limit lines. Variation that

is outside the stable statistical distribution, i.e. above the upper control

limit or below the lower control limit, is special

cause variation. The point for March

falls below the lower control limit. This means that the March data is special

cause variation. Special cause variation is the workers responsibility; they

typically know more about possible causes than the manager because they are

closer to the process. But the workers need training in problem solving to fix

special cause variation and they need to be empowered to make fixes to their

processes.

The workers should review the

data for March and examine the phone system to see if they can determine the

reason the daily averages were so low. For example, the phones may have been

out of order for a week, which would have lowered the daily expenses but

require no action other than getting the system operating again. Properly

trained and motivated workers can handle special cause problems, usually

without any management involvement.

A stable process is a good

candidate for process improvement. The goal of process improvement for a stable

process is to reduce the variation and/or change the mean. Process improvement

should not be attempted on a process that is unstable until the process is

brought to a stable condition because changes in data taken on an unstable

process cannot be uniquely attributed to the action of the process improvement.

The special cause variation that makes the process unstable must be removed

before beginning process improvement.

Note that the control chart

also provides the manager information useful in considering process

improvement. In the example shown in figure 18 the yearly average phone

expenses are about $21 per day. A manager can evaluate the cost benefit of

making a change to the phone service based on this data since it is stable over

a year. If the manager can make a change without investment that promises a 10%

reduction in phone expenses the manager can see that data will have to be

monitored for about four to six months to determine if the mean daily expenses

do indeed drop from $21 to $19 because the normal range of variation in monthly

averages is larger than the expected change. However, if the change really

works as promised then in about four to six months the monthly averages should

begin to vary about a new long term average and the control chart will show

this change.

Exercise

1. Go

to “Control Charts” in Wikipedia (http://en.wikipedia.org/wiki/Control_)

and read the article. This material expands upon the introduction given in this

lecture.

2. Go

to http://www.goalqpc.com/shop_products.cfm

and buy yourself a copy of Memory Jogger

II. This handy book teaches everything you need to know about problem

identification and problem analysis. It is small enough to carry in your pocket

and it is your guide to the details of process improvement. If you prefer a

spiral bound version it is available from Amazon.com (Michael Brassard, and

Diane Ritter, The Memory Jogger II: A

Pocket Guide of Tools for Continuous Improvement and Effective Planning)

There is also a Six Sigma Memory Jogger available.

The Memory

Jogger book recommended here is so widely used and so effective for the

practical user that there is no point in repeating the material in this course.

The student is expected to study the Memory Jogger and put the techniques into

practice. This means that the student

and all the people reporting to the student are to have the Memory Jogger book

, or an equivalent, be trained in the techniques summarized in the book and put

these techniques into practice. This is essential if an effective organization

is expected. The exception is if your organization is following the Six Sigma

approach where only selected people are highly trained.

If you prefer not having to learn statistical

techniques yourself you can attend training if your budget and schedule

permits. One example workshop in statistical process control is offered by the

American Supplier Institute. See: http://www.amsup.com/spc/1.htm. This workshop

focuses on manufacturing but the techniques work for any type of organization.

A web search reveals many other training organization offering similar

programs. I have found it more cost effective when training all workers to

bring the trainer to the organization rather than sending workers to outside

training.

If you find that the pace of blog posts

isn’t compatible with the pace you would

like to maintain in studying this material you can buy the book “The Manager’s Guide for Effective

Leadership” in hard copy or for

Kindle at:

or hard copy or for nook at:

or hard copy or E-book at: